What is Personal Income Tax in Nigeria?

Personal Income Tax is tax imposed on gain or profit from any trade, business, profession or vocation; or any salary, wage, fee, allowance or other gain or profit from employment of individuals.

What Law Enables Personal Income Tax in Nigeria?

Personal Income Tax (Amendment ) Act 2011.

Who Pays Personal Income Tax in Nigeria?

Personal Income Tax is paid by individuals who are either employed or running their own businesses under a business name or partnership and communities, families and any trustee or executor under any settlement, trust or estate deemed to be resident in the State at a particular year.

Does States' Board of Internal Revenue (SBIR) collect Personal Income Taxes?

Yes. SBIR collects Income Tax from the following set of Tax Payers:

(a.) Individuals in their various States of Residence,

(b.) Body of Individuals such as Communities/Families that run a business;

(c.) Business names and Partnerships;

(d.) Executors of estates of deceased persons and trustees of trusts.

Does Federal Inland Revenue Service (FIRS) collect Personal Income Taxes?

Yes. FIRS collects Income Tax from the following set of tax payers:

(a.) Persons employed in the Nigerian Army, the Nigerian Navy, the Nigerian Air Force and the Nigerian Police other than in a civilian capacity;

(b.) Body of individuals such as Communities/Families that run a business;

(c.) Officers of the Nigerian Foreign Service;

(d.) Non-residents who derive income or profit from Nigeria.

What is the Mode of Payment for Personal Income Taxes?

Tax on the income of Self-employed individuals or that of Communities, Families, Trustee or Executor is paid directly to the tax authorities while for Employed individuals, the employers deduct appropriate tax from the income of their employees and remit same to the tax authorities on monthly basis.

What are Consolidated Allowances in Personal Income Taxes?

A Consolidated Relief Allowance shall be granted on income at HIGHER of 1% of Gross Income or a flat Rate of N200,000.00 PLUS 20% of Gross Income.

What items are Tax-exempt from my emolument?

The following deductions are exempted from PITA.

(a.) National Housing Fund Contribution

(b.) National Health Insurance Scheme

(c.) Life Assurance Premium

(d.) National Pension Scheme

(e.) Gratuities

What are the rate for computing Personal Income Tax calculated in Nigeria?

After the relief allowance and exceptions had been granted, the balance of income shall be taxed as specified in the following Sixth Schedule Table:

(a.) First N300,000 at 7%

(b.) Next N300,000 at 11%

(c.) Next N500,000 at 15%

(d.) Next N500,000 at 19%

(e.) Next N1,600,000 at 21%

(f.) Above N3,200,000 at 24%

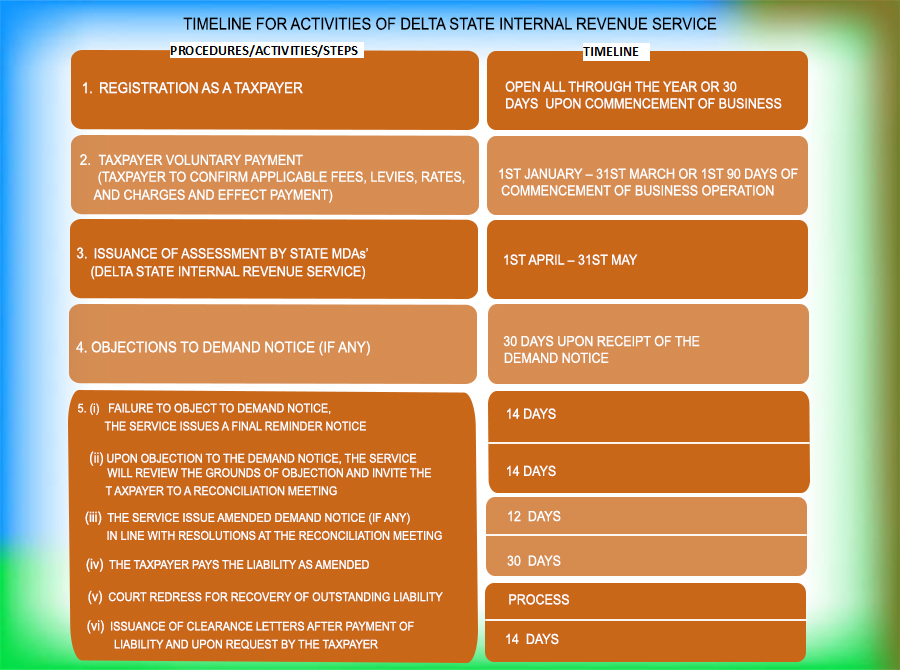

What is the deadline for submitting annual returns?

Every employer shall be required to file a return with the relevant tax authority of all emoluments paid to its employees, not later than 31st January of every year in respect of all employees in its employment in the preceding year.

Is there a penalty for failing to file my returns?

The penalty for failure to file returns according to the Personal Income Tax (Amendment) Act, 2011 is N500, 000 for corporate organisations and N50, 000 for individuals.

Are Religious Organizations liable to pay taxes?

No. The third schedule (section 19 (1) 74) Item 12 to Personal Income Tax Act CAP P8 LFN 2004 as amended “exempts the income of any ecclesiastical, charitable or educational institution of a public character from taxation provided the income is not derived from a trade or business carried on by such institution”.

The import of this provision is that incomes of the religious bodies from religious activities e.g. tithe, offerings, donations, are not taxable. The following are however taxable:

(a.) Income derived from business activities e.g. letting of properties, transportation, production and sales of Journals , Periodicals, Audio & Video CDs etc, where these activities are carried out in the name of a separate entity or for profit.

(b.) Where religious organisations’ funds are used to acquire assets i.e. motor vehicles, landed property etc. in a name different from that of the religious organisation or in the name of an individual who is associated with the religious organisation, funds so expended become income in the hand of the entity/individual and as such taxable.

What is Minimum Tax?

1% of Gross Income.

What is Self Assessment?

It is the ‘do it yourself’, easier and convenient approach recently introduced by DSIRS which enable a new Tax Payer to assess him/herself, make payment through any of the designated banks and obtain his/her e-TCC without visiting any Tax Office or Tax Officer.

What is difference between Pay As You Earn (PAYE) and Direct Assessment?

PAYE and Direct Assessment are two ways of assessing individuals to tax. PAYE is for individuals under paid employment and Direct Assessment is for Self Employed individuals.

How do I confirm if taxes deducted from my monthly emoluments are remitted to the state Government?

You can officially obtain information on all taxes paid on your behalf through the Executive Chairman of DSIRS.

Is a temporary or casual worker meant to pay taxes?

Yes. The Personal Income Tax (Amendment) Act, 2011 combined with the provisions of S.3 (1)(b) and S.3(1)(b)(i) particularly defining the taxpaying employee as either a temporary or permanent employee.

Is it compulsory for a full time house wife or jobless individual to pay taxes to Delta State Government?

Yes. The position of the law is that all adult from the age 18 and above must pay Personal Income Tax except those exempted by the law as stipulated in the Third Schedule of PITA 104 CAP P8 LFN 2004 & (Amendment) at 2011.

Can I use withholding taxes deducted on me to offset my Personal Income Tax Liability?

Yes. Withholding Taxes is recognized as part of taxes paid and can be net off from liability assessed for the year and balance is paid.

Can I pay under Self Assessment Approach?

No, for continuity and adequate record keeping, Tax payers who have tax records at any DSIRS office should approach the same office for proper assessment on yearly basis. This is important for proper coordination.

How do I file returns as a Self Employed?

As a self employed you can file returns following the below steps:

(a.) File your Annual Tax Returns with the Assessment Authority nearest to you, or approach the office for assistance if you do not know how to prepare the returns;

(b.) An Assessment Notice containing the amount of tax due for payment by you will given to you by the Assessment Authority after due assessment of the returns;

(c.) Pay the assessed amount to any branch of the designated banks and obtain Acknowledgement of Payment Slip in addition to the bank teller for the payment as evidence that you have paid to the correct government account;

(d.) Present the teller and the Acknowledgement of Payment Slip to the Assessment Authority that issued the Assessment Notice to obtain Revenue Receipt for your payment.

How do I file returns as an Employee (Taxpayer in employment)?

As an Employee (Taxpayer in employment) you can file returns following the below steps:

(a.) At the beginning of the year, file your Annual Income Declaration with the Assessment Authority nearest to you;

(b.) After due assessment, you will be given Annual Tax Estimate which will detail your expected income, reliefs granted and monthly Tax Estimates based on the information supplied in the Annual Income Declaration Form.

(c.) Present the Income/Tax Estimates to your employer who has the duty to deduct the monthly estimated tax and other tax that may accrue on additional income not declared in the Annual Income Declaration Form.

(d.) Your employer will remit tax deducted from your monthly income to the Internal Revenue Service by paying the deductions to any branch of the designated banks not later than the 10th of the month for previous month’s deduction;

(e.) Your employer will obtain Acknowledgement of Payment Slip in addition to the bank teller for the payment as evidence that the money was paid to the correct government account;

(f.) Your employer will present the teller and the Acknowledgement of Payment Slip to the Assessment Authority nearest to it to obtain Revenue Receipt for the payment.

What are the other Tax obligations of Religious Organization?

(a.) Pay as You Earn (PAYE): As employers of Labor, they are required to deduct appropriate tax from the income of their employees and pay same to Delta State Internal Revenue Service on or before 10th of the following month through any designated Delta State revenue collecting banks.

(b.) Withholding Tax: Whenever a Religious body pays an individual or an unincorporated entity Rent, Royalty, Management Fees, Consultancy Fees, Technical Service Fees, Agency Fees, Supplies and Contracts, appropriate withholding tax must be deducted and remitted to Delta State Internal Revenue Service through any of the designated Delta State revenue collecting banks.